Bank reconciliation is a critical process for any business that wants to maintain accurate financial records. In QuickBooks Online, reconciling your bank and credit card accounts ensures that your financial statements reflect the true state of your finances. Accurate reconciliations help prevent errors, detect fraud, and provide a clear view of your company’s cash flow.

[ez-toc]

Introduction: The Importance of Accurate Bank Reconciliations in QuickBooks Online

Why Reconciliation Matters

Reconciliation is the process of comparing your bank statements with your company’s accounting records to ensure that every transaction matches up. This includes verifying deposits, withdrawals, and any fees or interest charges. When reconciliations are done correctly, it guarantees that the balances in QuickBooks mirror those in your bank accounts, making your financial statements reliable.

A well-reconciled account means your financial data is accurate, which is essential for making informed business decisions. It also simplifies the preparation of tax returns and financial reports, as well as ensuring compliance with financial regulations. Furthermore, accurate reconciliations can highlight discrepancies such as unauthorized transactions or accounting errors that need to be addressed promptly.

Common Scenarios for Undoing or Unreconciling Transactions

While the goal is to always have accurate reconciliations, there are times when you may need to undo or unreconcile transactions. This can happen for several reasons:

- Mistakes in Data Entry: If a transaction was entered incorrectly, it might appear in the wrong place on your reconciliation. For example, you might have entered the wrong amount, or selected the wrong account. In such cases, undoing the reconciliation for that specific transaction allows you to correct the error without affecting the entire account.

- Duplicate Transactions: Sometimes, transactions may be duplicated in QuickBooks, leading to an inaccurate reconciliation. This can happen due to manual entry errors or issues with bank feeds. Identifying and removing these duplicates from your reconciliation is essential for maintaining accuracy.

- Bank Errors: Banks occasionally make errors, such as incorrect charges or deposits. If these errors are reflected in your bank statement and subsequently in your QuickBooks account, you’ll need to undo the reconciliation after the bank corrects the mistake.

- Unrecorded Transactions: If you discover transactions that were not recorded in QuickBooks but appear on your bank statement, you may need to add them and then reconcile again. This ensures that your financial records are complete and accurate.

- Adjustments or Corrections: At times, you might make adjustments or corrections after a reconciliation has been completed. This could include updating a transaction that was previously reconciled, which may require you to undo the reconciliation to make the necessary changes.

- Changes in Account Settings: If there have been changes to the settings of an account—such as modifications to account numbers or merging of accounts—previous reconciliations may need to be reviewed and potentially undone to reflect the new settings accurately.

- Partial Reconciliation: Sometimes, a partial reconciliation may be done for a specific period, and later, additional transactions need to be reconciled for the same period. In such cases, undoing the original reconciliation might be necessary to include all transactions.

- Year-End Adjustments: At the end of the fiscal year, adjustments may be made to your accounts for tax purposes or to align with financial reporting standards. These adjustments might require undoing previous reconciliations to ensure that all figures are accurate and up to date.

- Audits or Financial Reviews: During an audit or financial review, discrepancies might be found that necessitate the undoing of a reconciliation. This allows you to correct any errors before finalizing your financial statements.

- Switching Accounting Methods: If your business transitions from cash basis accounting to accrual accounting, or vice versa, you may need to review and potentially undo previous reconciliations to align with the new accounting method.

Step-by-Step Guide: Undoing an Entire Reconciliation in QuickBooks Online Accountant

Undoing a bank reconciliation in QuickBooks Online Accountant is a straightforward process. Here’s how you can do it:

-

Sign in to QuickBooks Online Accountant.

- Make sure you have the necessary permissions to access and manage the client’s reconciliation records.

- Access the Client’s Account:

- Navigate to your client’s QuickBooks account that requires the reconciliation to be undone.

- Go to the Accounting Menu:

- On the left-hand side, click on the Accounting menu and select Reconcile. This will take you to the reconciliation page where you can see all the reconciliations that have been completed for various accounts.

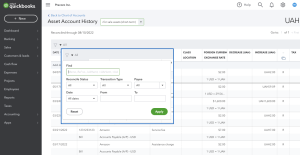

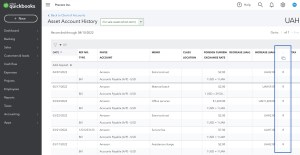

- View Reconciliation History:

- In the Reconcile section, click on History by account. This will display a list of all the reconciliations that have been performed for that account, along with their dates and the status.

- Select the Account and Date Range:

- Choose the account you want to work with and select the relevant date range to locate the specific reconciliation you need to undo.

- Locate the Reconciliation:

- Find the reconciliation in question from the list. Make sure it is the correct reconciliation you want to undo.

- Undo the Reconciliation:

- In the Action column, there will be a drop-down menu next to the reconciliation. Click on it and select Undo. QuickBooks will prompt you with a confirmation message asking if you’re sure you want to undo the reconciliation.

- Confirm the Action:

- Click Yes to confirm. QuickBooks will then proceed to undo the entire reconciliation. This action cannot be undone, so it’s crucial to double-check that you’ve selected the right reconciliation.

- Review the Changes:

- After undoing, review the account to ensure that everything is as expected. You may need to re-reconcile the account if additional changes are required.

-

How to Undo Reconciliation in QuickBooks Online: A Step-by-Step Guide

Key Considerations: Impact on Subsequent Reconciliations and Best Practices

Undoing a reconciliation is a significant action that can affect your financial records in several ways. Here are some key considerations:

- Impact on Subsequent Reconciliations:

- When you undo a reconciliation, it affects all subsequent reconciliations. This means any reconciliations done after the one you’re undoing will also be affected. You may need to redo those reconciliations to ensure that your financial records remain accurate.

- Reviewing Adjustments:

- If there were any adjustments or changes made during the reconciliation process, these will also be undone. It’s essential to review and possibly re-enter any adjustments to maintain the accuracy of your financial data.

- Best Practices:

- Document the Changes: Always document why you’re undoing a reconciliation. This helps maintain a clear audit trail and provides context for any future reviews.

- Backup Your Data: Before making significant changes like undoing a reconciliation, it’s advisable to back up your QuickBooks data. This provides a safety net in case something goes wrong.

- Consult with an Accountant: If you’re unsure about the implications of undoing a reconciliation, it’s a good idea to consult with an accountant or QuickBooks expert. They can provide guidance and help ensure that your records remain accurate and compliant.

- Re-Reconcile Carefully:

- After undoing a reconciliation, take your time to go through the account and reconcile it again. Ensure that all transactions are accurate and that there are no discrepancies.

- Understand the Long-Term Impact:

- Undoing a reconciliation can have long-term effects on your financial reporting. It may impact your tax filings, financial statements, and overall business decisions. Ensure that the action is necessary and that you’re fully aware of its consequences.

By following these steps and considerations, you can successfully undo a bank reconciliation in QuickBooks Online while maintaining the integrity of your financial data.

Step-by-Step Instructions: Changing the Reconciliation Status of Individual Transactions

If you need to unreconcile specific transactions in QuickBooks Online, follow these steps:

- Sign in to QuickBooks Online:

- Ensure you have the necessary permissions to make changes to reconciled transactions.

- Access the Chart of Accounts:

- From the left-hand menu, go to Accounting and select Chart of Accounts.

- Select the Account:

- Choose the account containing the transaction you want to unreconcile, and click View register.

- Locate the Transaction:

- Scroll through the register to find the transaction you need to unreconcile.

- Change the Reconciliation Status:

- Click on the “R” (Reconciled) status next to the transaction. This will toggle the status to either “C” (Cleared) or blank, depending on your needs:

- R: Reconciled

- C: Cleared

- Blank: Neither cleared nor reconciled

- Click on the “R” (Reconciled) status next to the transaction. This will toggle the status to either “C” (Cleared) or blank, depending on your needs:

- Save the Changes:

- After adjusting the status, click Save and confirm the changes when prompted.

Important Tips: Ensuring Your Reconciled Balances Remain Accurate

- Double-Check Before Unreconciling:

- Before you unreconcile a transaction, review your records to ensure it’s necessary. Unreconciling can affect your balances, so be certain that it’s required.

- Reconcile After Changes:

- After making changes, run a reconciliation for the affected period to ensure that your balances match your bank statement. This step helps maintain the accuracy of your financial records.

- Document Your Actions:

- Keep a record of why you made changes to reconciled transactions. This documentation is helpful for audits and for explaining any discrepancies in future financial reviews.

- Backup Your Data:

- Before making significant changes like unreconciling transactions, consider backing up your QuickBooks data to prevent data loss in case of errors.

- Consult with an Accountant:

- If you’re unsure about the impact of unreconciling transactions, it’s wise to consult with an accountant. They can offer guidance and ensure that your financial data remains accurate and compliant with accounting standards.

By following these steps and tips, you can safely unreconcile specific transactions in QuickBooks Online while ensuring that your reconciled balances remain accurate.

Conclusion

Maintaining accurate bank reconciliations in QuickBooks Online is essential for ensuring the integrity and reliability of your financial records. Bank reconciliation is a vital process for any business, as it ensures that your accounting records align with your actual bank statements. This alignment helps prevent errors, detect potential fraud, and offer a clear picture of your company’s financial status. When reconciliations are conducted correctly, they contribute significantly to the accuracy of your financial reports and statements, which are crucial for informed decision-making and effective financial management.

Proper reconciliation involves comparing every transaction recorded in QuickBooks with those listed in your bank statement. This process includes verifying all deposits, withdrawals, fees, and interest charges. When discrepancies arise, such as errors in data entry or duplicate transactions, it’s important to address them promptly to maintain accurate financial records.

In QuickBooks Online, the steps to undo, unreconcile, or remove transactions are designed to help you correct errors and ensure that your financial data remains accurate. Understanding when and how to perform these actions is crucial. For instance, you may need to undo a reconciliation if you’ve identified mistakes or discrepancies in your records. This process involves a series of steps to ensure that your reconciliation status is adjusted correctly. Similarly, if you need to unreconcile specific transactions, QuickBooks Online provides a straightforward method to change the reconciliation status of individual entries.

By carefully following the provided steps for undoing and unreconciling transactions, you can address issues such as incorrect data entry, duplicate transactions, and bank errors. It’s important to proceed with these actions methodically, ensuring that each step is executed correctly to avoid further complications. For instance, when undoing an entire reconciliation, you should double-check that you’ve selected the correct reconciliation to avoid affecting subsequent reconciliations. Similarly, when unreconciling individual transactions, ensure that you accurately change the reconciliation status to maintain the integrity of your account balances.

Despite these tools and processes available within QuickBooks Online, there are instances where professional advice may be beneficial. If you encounter complex situations, such as significant discrepancies or issues related to changes in accounting methods, consulting with an accountant or QuickBooks expert is highly recommended. Their expertise can help navigate challenging reconciliation issues, provide insights into the implications of your actions, and ensure that your financial records are compliant with accounting standards and regulations.

Professional accountants and QuickBooks experts can offer valuable guidance in scenarios where the implications of undoing or unreconciling transactions are not immediately clear. They can help you understand the potential impact on subsequent reconciliations, provide advice on best practices for documenting changes, and assist in maintaining a clear audit trail. Additionally, their expertise can help you avoid common pitfalls and ensure that your financial data remains accurate and reliable.

In summary, effective bank reconciliation management in QuickBooks Online is a critical component of maintaining accurate and trustworthy financial records. By following the detailed steps for undoing, unreconciling, and removing transactions, you can address discrepancies and ensure that your financial statements reflect the true state of your company’s finances. However, when faced with complex issues or uncertainties, seeking professional advice is always a prudent step to ensure the accuracy and compliance of your financial records.

Incorporating these practices into your regular financial management routine will help safeguard the accuracy of your financial data, support informed decision-making, and contribute to the overall financial health of your business. Proper reconciliation not only helps in preventing errors but also serves as a tool for detecting fraud and maintaining a clear understanding of your company’s financial position. As you manage your bank reconciliations, remember the importance of accuracy and thoroughness in maintaining reliable financial records.

FAQs: Detailed Answers to Common Questions about Undoing Reconciliations and Best Practices

- What are the common reasons for needing to undo a reconciliation in QuickBooks Online?

Undoing a reconciliation in QuickBooks Online may be necessary for several reasons, each with its own set of circumstances and solutions:

- Data Entry Errors: Mistakes in entering transactions, such as incorrect amounts or dates, can affect your reconciliation. If a transaction was recorded incorrectly, it might not match your bank statement, necessitating an undo to correct the error.

- Duplicate Transactions: Duplicate entries, whether from manual input or bank feed errors, can skew reconciliation. Identifying and removing these duplicates is crucial for accurate financial records.

- Bank Errors: Occasionally, banks make errors, such as incorrect charges or missing deposits. If these errors appear in your QuickBooks reconciliation, you may need to undo the reconciliation after the bank corrects the mistake.

- Unrecorded Transactions: Transactions that appear on your bank statement but are missing from QuickBooks require reconciliation adjustments. You may need to add these transactions and then reconcile again to ensure all entries are accounted for.

- Adjustments or Corrections: After completing a reconciliation, you might need to make adjustments or corrections to previously reconciled transactions. Undoing the reconciliation allows you to make these necessary changes.

- Changes in Account Settings: Changes such as merging accounts or modifying account numbers can impact previous reconciliations. Reviewing and potentially undoing reconciliations may be necessary to align with new account settings.

- Partial Reconciliation: A partial reconciliation done for a specific period may need to be undone if additional transactions are later discovered and need reconciliation for the same period.

- Year-End Adjustments: Year-end adjustments for tax purposes or financial reporting may require undoing previous reconciliations to ensure that figures are accurate and up-to-date.

- Audits or Financial Reviews: During audits or financial reviews, discrepancies might be identified that necessitate undoing a reconciliation to correct errors before finalizing financial statements.

- Switching Accounting Methods: Transitioning from cash basis to accrual accounting, or vice versa, may require reviewing and potentially undoing previous reconciliations to align with the new accounting method.

- How do I undo a reconciliation in QuickBooks Online Accountant?

Undoing a reconciliation in QuickBooks Online Accountant involves a series of steps to ensure accuracy and completeness. Here’s a detailed guide:

- Sign in to QuickBooks Online Accountant:

-

- Ensure you have the necessary permissions to access and manage reconciliation records.

- Access the Client’s Account:

-

- Navigate to the client’s QuickBooks account where the reconciliation needs to be undone.

- Go to the Accounting Menu:

-

- On the left-hand menu, click on “Accounting” and select “Reconcile” to access the reconciliation page.

- View Reconciliation History:

-

- Click on “History by account” to see a list of all reconciliations performed for the account, including dates and statuses.

- Select the Account and Date Range:

-

- Choose the account and date range to locate the specific reconciliation you want to undo.

- Locate the Reconciliation:

-

- Find the specific reconciliation from the list. Verify that you have selected the correct one.

- Undo the Reconciliation:

-

- In the Action column, click on the drop-down menu next to the reconciliation and select “Undo.” QuickBooks will prompt you with a confirmation message.

- Confirm the Action:

-

- Click “Yes” to confirm. QuickBooks will undo the entire reconciliation. This action is irreversible, so double-check that you’ve selected the right reconciliation.

- Review the Changes:

-

- After undoing, review the account to ensure that everything is accurate. You may need to re-reconcile the account if additional changes are required.

- What are the impacts of undoing a reconciliation on subsequent reconciliations?

Undoing a reconciliation affects all subsequent reconciliations. Here’s how:

- Adjustment of Subsequent Reconciliations: Any reconciliations completed after the one you undo will be impacted. You may need to review and redo these reconciliations to reflect accurate balances and transactions.

- Reviewing Adjustments: Adjustments made during the reconciliation process will be undone, so you may need to re-enter or correct these adjustments to maintain accurate financial data.

- Potential Errors: If subsequent reconciliations were based on the incorrect reconciliation, undoing it might reveal or create new errors that need to be addressed.

- How do I unreconcile individual transactions in QuickBooks Online?

Unreconciling individual transactions is a simpler process compared to undoing an entire reconciliation. Follow these steps:

- Sign in to QuickBooks Online:

-

- Ensure you have the permissions required to make changes to reconciled transactions.

- Access the Chart of Accounts:

-

- From the left-hand menu, select “Accounting” and then “Chart of Accounts.”

- Select the Account:

-

- Choose the account containing the transaction you wish to unreconcile, and click “View register.”

- Locate the Transaction:

-

- Scroll through the register to find the transaction you need to unreconcile.

- Change the Reconciliation Status:

-

- Click on the “R” (Reconciled) status next to the transaction. This will toggle the status to either “C” (Cleared) or leave it blank, depending on your needs:

- R: Reconciled

- C: Cleared

- Blank: Neither cleared nor reconciled

- Click on the “R” (Reconciled) status next to the transaction. This will toggle the status to either “C” (Cleared) or leave it blank, depending on your needs:

- Save the Changes:

-

- After adjusting the status, click “Save” and confirm the changes when prompted.

- What are the best practices for managing reconciliations and ensuring accurate financial records?

Adhering to best practices for managing reconciliations ensures the accuracy and reliability of your financial records. Here are some key best practices:

- Document Your Actions: Always keep detailed records of why reconciliations were undone or transactions were unreconciled. This documentation provides context for any future reviews or audits.

- Backup Your Data: Before making significant changes like undoing a reconciliation, back up your QuickBooks data. This precaution helps protect against data loss in case of errors.

- Consult with an Accountant: If you’re unsure about the implications of undoing a reconciliation or making other adjustments, seek advice from an accountant or QuickBooks expert. They can provide guidance and ensure compliance with accounting standards.

- Reconcile Carefully: After making changes, take your time to thoroughly review and reconcile the affected period. Ensure that all transactions are accurate and that no discrepancies remain.

- Understand the Long-Term Impact: Recognize that undoing a reconciliation can have long-term effects on financial reporting, tax filings, and business decisions. Make sure you fully understand these consequences before proceeding.

- Regular Reconciliation Schedule: Maintain a regular schedule for reconciling your accounts to prevent errors from accumulating. Frequent reconciliations help catch and correct issues early.

- Use Reconciliation Reports: Utilize QuickBooks Online’s reconciliation reports to review discrepancies and ensure that your reconciliations are accurate.

- How do I handle reconciliation discrepancies identified during an audit or financial review?

Discrepancies identified during an audit or financial review should be handled systematically:

- Investigate the Discrepancies: Carefully review the discrepancies to understand their source. This may involve checking transaction records, comparing bank statements, and verifying data entry.

- Correct the Errors: Once you’ve identified the cause of the discrepancies, make the necessary corrections in QuickBooks. This might include adjusting transactions, updating reconciliation statuses, or undoing and redoing reconciliations.

- Document the Corrections: Keep detailed records of the corrections made, including the reasons for the changes and the steps taken to resolve the issues.

- Review and Reconcile: After making corrections, review and reconcile the affected periods to ensure that all changes have been accurately reflected.

- Consult with a Professional: If the discrepancies are complex or involve significant amounts, consult with an accountant or QuickBooks expert for guidance on resolving the issues and ensuring compliance.

- What should I do if I find errors in reconciliations from previous fiscal years?

Errors in reconciliations from previous fiscal years require careful handling:

- Review the Errors: Identify and understand the nature of the errors. This may involve examining historical reconciliation records and bank statements.

- Correct the Reconciliations: Make the necessary adjustments to the reconciliations. This might involve undoing and redoing reconciliations for the affected periods.

- Adjust Financial Statements: If the errors have impacted financial statements or tax filings, update these documents accordingly to reflect the correct information.

- Consult with an Accountant: For errors involving previous fiscal years, it’s advisable to consult with an accountant. They can provide guidance on the implications for financial statements and tax filings and help ensure compliance with accounting standards.

- Document Changes: Keep thorough records of the corrections made and the reasons for the changes. This documentation is important for future reference and audits.

- How can I prevent reconciliation errors from occurring in the future?

Preventing reconciliation errors involves implementing proactive measures and best practices:

- Ensure Accurate Data Entry: Double-check transaction entries for accuracy before reconciling. Implement controls to minimize data entry errors.

- Regularly Review Transactions: Frequently review transactions to identify and address issues before they affect reconciliations.

- Utilize Bank Feeds: Use bank feeds to import transactions directly into QuickBooks, reducing the risk of manual entry errors.

- Educate Staff: