What's the Difference Between

Accrual and Cash Accounting?

A complete 2026 guide for small business owners on choosing the right accounting method — with real examples, comparison tables, and expert recommendations.

By CashBook Accounting Team | May 2026 | 9 min read

📌 Article Summary

Cash accounting records income and expenses only when money physically changes hands — it's simple, intuitive, and ideal for tiny businesses. Accrual accounting records revenue when it's earned and expenses when they're incurred, regardless of when cash moves — making it far more accurate for measuring true profitability. This guide compares both methods across cost, complexity, tax impact, IRS requirements, and suitability — so you can make a confident, informed decision about which accounting basis is right for your business stage in 2026 and beyond.

📚 Table of Contents

- Why Your Accounting Method Matters

- Cash vs Accrual: Core Definitions

- How Each Method Works in Practice

- Head-to-Head Comparison: 10 Key Factors

- Real Transaction Examples Side by Side

- IRS Rules & Legal Requirements in 2026

- Pros and Cons of Each Method

- Who Should Use Which Method?

- How to Switch From Cash to Accrual

- Frequently Asked Questions

- Related Articles

1. Why Your Accounting Method Matters

The accounting method your business uses isn't just a technical detail — it fundamentally shapes how your financial statements look, how much tax you owe in a given year, whether you can qualify for loans, and whether your reported profit actually reflects your business's financial reality. Choosing the wrong method can lead to inaccurate financial pictures, unexpected tax bills, and even IRS penalties.

In 2026, the IRS has specific rules on which businesses must use accrual accounting, and which can elect cash basis. These thresholds matter — and crossing them without switching your accounting method is a compliance violation. If your books were set up on the wrong basis, our bookkeeping clean-up services can diagnose and correct the issue before it becomes costly.

Understanding both methods — not just the one you currently use — also makes you a sharper financial decision-maker. When you review a financial statement, apply for credit, or assess whether a month was actually profitable, the accounting method behind those numbers determines how truthful they are. Getting this right is foundational, as outlined in our guide to setting up your first bookkeeping system.

Not Sure Which Method Your Books Use?

Our experts at CashBook Accounting will review your books and set you up on the right accounting basis — fast and stress-free.

IRS gross receipts threshold requiring accrual accounting for most businesses

Accounting methods accepted by the IRS for small business tax reporting

of small businesses under $1M revenue use cash-basis accounting

Generally Accepted Accounting Principles require accrual basis for public companies

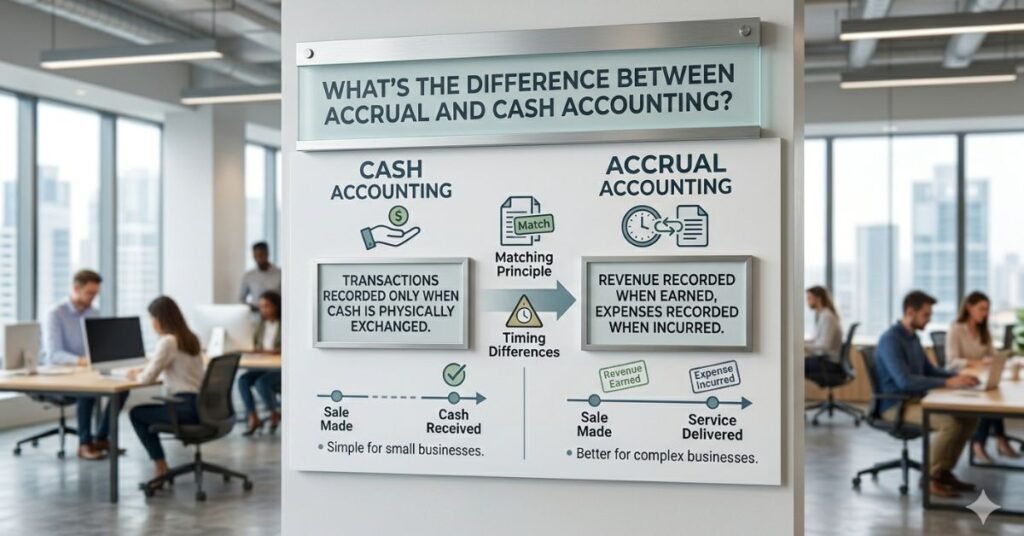

2. Cash vs Accrual: Core Definitions

Before diving into comparisons, let's establish clear definitions of each method. These definitions are the lens through which every transaction in your books is recorded.

Records transactions only when cash is received or paid. Simple, immediate, and easy to manage without an accountant.

- Revenue recorded when payment received

- Expenses recorded when bill is paid

- Matches your bank statement closely

- Doesn't account for receivables/payables

- Best for: Sole traders, freelancers, micro-businesses

- Also known as: Cash basis, cash method

Records revenue when earned and expenses when incurred, regardless of when cash actually moves. Gives a true picture of financial health.

- Revenue recorded when work is completed/invoice sent

- Expenses recorded when obligation is incurred

- Requires tracking accounts receivable & payable

- Compliant with GAAP and IFRS standards

- Best for: Growing businesses, inventory holders, corporations

- Also known as: Accrual basis, accruals method

3. How Each Method Works in Practice

The distinction between the two methods becomes crystal clear when you walk through a single scenario under both systems. Let's use a consulting business that completes a $5,000 project in November, sends an invoice on November 30, and receives payment on January 15 of the following year.

| Date | Event | 💵 Cash Accounting Records | 📊 Accrual Accounting Records |

|---|---|---|---|

| Nov 30 | Project completed, invoice sent | Nothing recorded | Revenue: +$5,000 |

| Nov 30 | Accounts receivable created | Not tracked | AR: +$5,000 (Asset) |

| Jan 15 | Client pays invoice | Revenue: +$5,000 | AR cleared; Cash +$5,000 |

| Year-End Impact | Which year does $5K appear in? | Next year (Jan) | This year (Nov) |

The Real-World Implication: Under cash accounting, this business's November P&L shows zero revenue for a completed project. Under accrual, it shows the full $5,000 earned. If management decisions, bonus calculations, or loan applications depend on monthly financials, the cash method gives a dangerously distorted picture of performance.

4. Head-to-Head Comparison: 10 Key Factors

Here is a comprehensive comparison across the dimensions that matter most to small business owners making this decision in 2026:

| # | Factor | 💵 Cash Accounting | 📊 Accrual Accounting | Better For… |

|---|---|---|---|---|

| 1 | Complexity | Very simple — just track cash in/out | More complex — tracks receivables, payables, deferred items | Cash: Simplicity |

| 2 | Accuracy of P&L | Reflects cash flow, not true profit | Accurately reflects earned revenue and incurred costs | Accrual: Accuracy |

| 3 | Startup Cost | Near zero — no specialist needed | Higher — typically requires bookkeeper or accountant | Cash: Low cost |

| 4 | Tax Planning | Can defer income by delaying invoicing | Tax based on earned revenue — harder to defer | Cash: Flexibility |

| 5 | GAAP Compliance | Not GAAP-compliant | Fully GAAP and IFRS compliant | Accrual: Compliance |

| 6 | Investor/Lender Appeal | Not acceptable for most investors | Required by banks, investors, and VCs | Accrual: Funding |

| 7 | Inventory Tracking | Doesn't match revenue to inventory costs | Properly matches COGS to revenue period | Accrual: Inventory |

| 8 | IRS Requirement | Allowed below $30M gross receipts | Required above $30M; required for C-corps | Depends on size |

| 9 | Cash Flow Visibility | Perfectly mirrors real cash position | Profit may not match actual cash available | Cash: Cash clarity |

| 10 | Scalability | Breaks down with growth and complexity | Scales with any business size and structure | Accrual: Growth |

5. Real Transaction Examples Side by Side

Let's walk through three common business scenarios and see how each method records them differently — illustrating why the method choice has such significant financial reporting implications.

🔁 Scenario A: $8,000 Service Contract — Work Done in March, Paid in April

💵 Cash Method

📊 Accrual Method

🔁 Scenario B: $2,400 Annual Insurance Premium Paid Upfront in January

💵 Cash Method

📊 Accrual Method

🔁 Scenario C: $500 Utility Bill Incurred in December, Paid January

💵 Cash Method

📊 Accrual Method

6. IRS Rules & Legal Requirements in 2026

The IRS does not leave accounting method choice entirely up to the business. There are specific rules that mandate which method certain businesses must use — and failing to comply is a tax code violation that can result in back taxes, interest, and penalties.

| Business Type / Threshold | Required Method | IRS Code Reference |

|---|---|---|

| Gross receipts ≤ $30M (3-yr avg) | May use Cash or Accrual | IRC §448 — Tax Cuts & Jobs Act threshold |

| Gross receipts > $30M (3-yr avg) | Must use Accrual | IRC §448(c) |

| C-Corporations (most sizes) | Must use Accrual | IRC §448(a)(1) |

| Partnerships with C-Corp partners | Must use Accrual | IRC §448(a)(2) |

| Tax shelters (any size) | Must use Accrual | IRC §448(a)(3) |

| Businesses with inventory (UNICAP) | Generally Accrual for inventory | IRC §471, §263A |

| Qualified Personal Service Corps | May use Cash regardless of size | IRC §448(b)(2) |

Switching Methods Requires IRS Approval: Changing from cash to accrual (or vice versa) requires filing Form 3115 (Application for Change in Accounting Method) with the IRS. This isn't optional — an unauthorized method switch can result in an adjustment to your taxable income and potential penalties. Our tax preparation team can manage this process for you, including calculating the Section 481(a) adjustment required on the transition year return.

7. Pros and Cons of Each Method

💵 Cash Accounting — Advantages

- Simplicity: Easy to understand and manage without accounting expertise — ideal for business owners who do their own books.

- Real cash visibility: Your bank balance closely matches your reported income — no surprises from unpaid invoices showing as profit.

- Tax timing control: You can legally defer income by delaying invoicing, or accelerate deductions by paying expenses before year-end.

- Lower bookkeeping cost: No need to track accounts receivable, accounts payable, or accruals — fewer transactions to manage.

💵 Cash Accounting — Disadvantages

- Distorted profitability: A profitable month looks bad if clients haven't paid yet; a slow month looks great if you collected old receivables.

- Limits funding options: Banks, investors, and the SBA generally require accrual-basis financial statements for loan and investment applications.

- Not GAAP-compliant: You cannot prepare audited GAAP financials on a cash basis — required for many contracts and public company reporting.

- Inventory mismatch: Revenue and cost of goods sold are not matched to the same period, making margin analysis unreliable.

📊 Accrual Accounting — Advantages

- True profitability picture: Revenue and expenses are matched to the period they relate to, giving an accurate view of business performance.

- GAAP & IFRS compliant: Required for audited financials, public companies, most lenders, and enterprise contracts.

- Better for growth planning: Accrual-basis financials support reliable budgeting, forecasting, and financial modeling.

- Inventory accuracy: Properly matches COGS to the period the goods were sold, enabling accurate gross margin analysis.

📊 Accrual Accounting — Disadvantages

- More complex: Requires tracking receivables, payables, prepaid expenses, accruals, and deferred revenue — typically needs professional bookkeeping.

- Cash flow disconnect: You may show strong profits on paper while having very little actual cash — a dangerous situation if not monitored separately.

- Higher bookkeeping cost: Requires more entries, more accounts, and more professional oversight — raising monthly bookkeeping expenses.

📊 Usage by Business Revenue Stage

Let CashBook Set Up the Right Accounting Method for You

From books clean-up to financial planning and tax preparation — our experts ensure your accounting method is correct, compliant, and optimized for your business stage.

8. Who Should Use Which Method?

The right accounting method depends on your business size, structure, growth stage, and whether you have inventory or investors. Use this decision framework to identify the right choice for your situation:

🧭 Accounting Method Decision Guide

| Business Profile | Recommended Method | Key Reason |

|---|---|---|

| Freelancer / solo consultant | Cash | Simple, low volume, no inventory |

| Service business under $500K | Cash (or hybrid) | Manageable without specialist |

| E-commerce / product business | Accrual | Inventory matching required |

| Business seeking a loan or investor | Accrual | GAAP compliance needed |

| Growing business $500K–$5M | Accrual | Accurate reporting for decisions |

| C-Corporation (any size) | Accrual (required) | IRS mandate |

| Payroll-heavy business | Accrual | Accrued wages matching required |

For e-commerce businesses with multi-platform inventory, our eCommerce bookkeeping services set up the correct accrual system from day one, ensuring proper COGS matching and sales tax compliance. Also see our expense tracking guide for tools that work under both methods.

9. How to Switch From Cash to Accrual Accounting

Switching accounting methods is more involved than simply changing a setting in your software. The IRS requires a formal process, and your books need to be restated properly to avoid double-counting income or deductions during the transition year.

| Step | Action Required | Notes |

|---|---|---|

| 1 | Determine your "cut-off" date | Most businesses switch at the start of a new fiscal year |

| 2 | Identify all accounts receivable | List all invoices sent but not yet paid as of the switch date |

| 3 | Identify all accounts payable | List all bills received but not yet paid as of the switch date |

| 4 | Identify prepaid expenses | Any payments made for future periods (insurance, rent) become assets |

| 5 | Calculate Section 481(a) adjustment | Net difference between cash and accrual income — reported over 1 or 4 years |

| 6 | File IRS Form 3115 | Required for all voluntary accounting method changes |

| 7 | Update your bookkeeping software | Switch accounting basis in QuickBooks, Xero, or your platform |

| 8 | Reconcile opening balances | Ensure all AR, AP, and prepaid accounts are entered correctly |

Don't Switch Alone. The IRS Section 481(a) adjustment is the most complex part of the transition — it requires recalculating income that was deferred or double-counted across the boundary year. An error here can result in an underpayment penalty. Our tax preparation team handles Form 3115 filings and 481(a) calculations accurately. For ongoing reconciliation after the switch, see our reconciliation guide and make sure you have the right documents for your bookkeeping in order.

Ready to Get Your Accounting Method Right?

From books clean-up to financial modeling and payroll services — CashBook Accounting is your complete financial partner for 2026 and beyond.

10. Frequently Asked Questions

11. Related Articles

© 2026 CashBook Accounting & Consultancy — Empowering Small Businesses with Expert Financial Management.